Should Congressional Pay Depend on Federal Budget Surpluses?

A public administration lens on incentive-based proposals for legislative compensation and fiscal accountability

By Max SheltonReviewed by PAP Editoral TeamUpdated July 25, 202625+ min read

What you’ll learn in this article…

The 27th Amendment requires that any law changing congressional pay cannot take effect until after an intervening election.

Only four federal budget surpluses have occurred in the last 60 years, all between 1998 and 2001.

No legislature in the developed world currently ties member pay or bonuses to fiscal surplus performance.

Proposed bonuses could reach millions per legislator annually, raising collective action and perverse incentive concerns.

Federal debt now exceeds $37 trillion, with interest payments alone consuming 14 percent of federal spending, and the Social Security trust fund projected to run dry in the early 2030s. Against that backdrop, a proposal circulating on Reddit and fixtheincentives.com suggests paying members of Congress millions in bonuses when the federal government achieves a budget surplus.

The idea is a textbook exercise in applied incentive design: if self-interest drives legislative behavior, then tying compensation to fiscal outcomes should redirect congressional priorities toward sustainable budgeting. For students and professionals in public administration and public policy, the proposal offers a case study in whether legislative inaction on fiscal sustainability stems from misaligned institutional incentives or from voter preferences that reward short-term spending and tax cuts.

How congressional pay is currently determined, what the surplus-linked bonus pool would look like in practice, and whether the Constitution even permits such a system illuminate larger questions about legislative behavior, accountability, and the design of democratic institutions.

How Congressional Pay Is Currently Determined

Congressional compensation comes directly from the Treasury of the United States, a requirement established in Article I, Section 6 of the Constitution. This foundational provision answers a straightforward question: members of Congress receive a salary paid by the federal government, not by their states or any outside entity. As of 2026, rank-and-file members of both the House and Senate earn $174,000 annually,1 a figure that has remained unchanged for nearly two decades despite mechanisms designed to adjust it.

The Ethics Reform Act of 1989 and Automatic Adjustments

The Ethics Reform Act of 1989 established an automatic cost-of-living adjustment (COLA) for congressional salaries, pegged to the Employment Cost Index. Under this system, pay would increase annually without requiring members to cast a politically uncomfortable vote to raise their own compensation. The design reflected a practical compromise: lawmakers would receive modest, inflation-linked adjustments while avoiding the appearance of self-dealing.

In practice, however, this automatic mechanism has been overridden repeatedly. Since 2009, Congress has blocked its own COLA through annual appropriations riders in 17 consecutive years.2 The proposed 3.8 percent increase in 2024, which would have added approximately $6,600 to member salaries, was denied like all the others before it.2 This pattern demonstrates that while the COLA framework exists on paper, Congress effectively self-regulates downward through legislative action each fiscal year.

The 27th Amendment's Timing Restriction

Any proposal to restructure congressional pay must contend with the 27th Amendment, ratified in 1992. This amendment prohibits any law varying congressional compensation from taking effect until an intervening election has occurred. The restriction exists to prevent sitting legislators from immediately benefiting from pay increases they approve for themselves.

For reformers considering surplus-linked bonuses or other performance-based compensation models, this constitutional requirement creates a significant delay. Any new pay structure could not apply to the Congress that enacted it. Members would be designing incentives for their successors, which may reduce political appetite for creative compensation reforms. Understanding what public policy actually is helps clarify why such structural constraints so often shape the boundaries of reform proposals.

The Gap Between Design and Reality

The disparity between the automatic COLA mechanism and actual congressional pay reveals important dynamics for public administration students to observe. The system was designed to depoliticize compensation decisions, yet members have consistently chosen to freeze their own pay, often citing fiscal concerns or public perception. Recent litigation has even produced a preliminary ruling favorable to lawmakers who argue the repeated COLA denials may violate the established adjustment framework.2 This tension between statutory design and political behavior offers a case study in how institutions can formally adopt one approach while informally pursuing another through appropriations power.

The Surplus-Linked Pay Proposal Explained

Designing incentive structures that align legislative behavior with long-term fiscal outcomes is a persistent challenge in public administration, and a proposal circulating under the banner of fixtheincentives.com offers one unusually direct answer: pay members of Congress more when the federal government actually runs a surplus.

The Core Mechanics

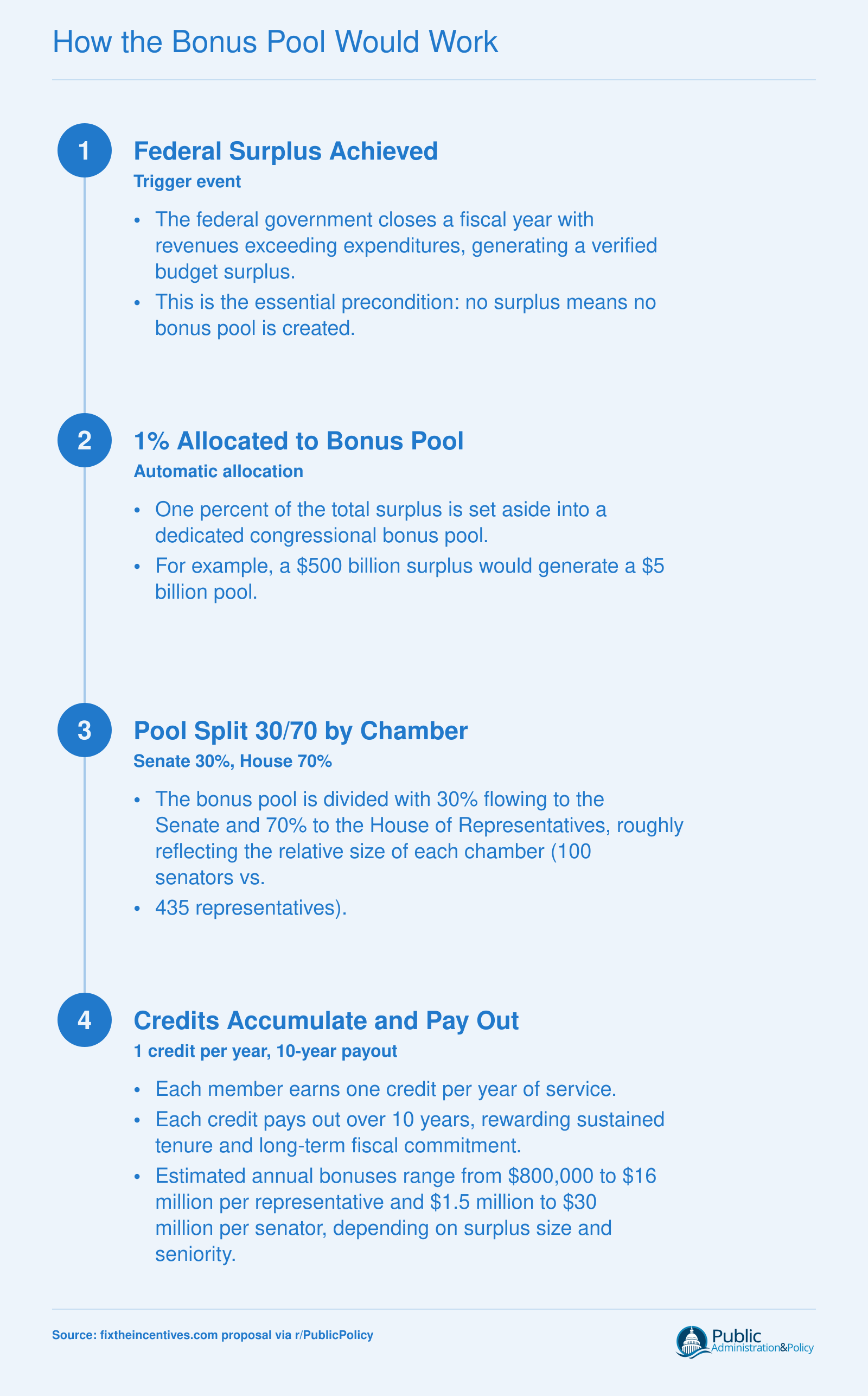

The mechanics are straightforward by design. Whenever the federal government closes a fiscal year with a surplus, 1% of that surplus flows into a bonus pool. That pool is then divided between the two chambers: 30% goes to the Senate and 70% to the House of Representatives. The split reflects the House's constitutional primacy over revenue and appropriations bills, where budget negotiations effectively begin.

The bonus pool does not simply get divided equally among members in the year it is earned. Instead, the proposal uses a credit system to extend the incentive across an entire legislative career.

The Credit System and the Long-Tail Incentive

Each member of Congress earns one credit for every year of service. Crucially, each credit pays out for ten years. That structure means a representative who helps produce a surplus early in a career continues receiving a share of that payout for a decade, while also accumulating new credits over time. The result is a compounding, long-tail incentive rather than a one-time bonus. From a behavioral standpoint, this is deliberate: the proposal attempts to reward sustained fiscal discipline rather than a single favorable budget cycle.

What Members Could Actually Earn

The estimated payout ranges are the part of this proposal that stops most readers cold. Senators could receive somewhere between $1.5 million and $30 million per year in bonus compensation. Representatives, drawing from the larger 70% pool but sharing it among a larger membership, could see between $800,000 and $16 million per year. Those figures dwarf the current congressional base salary of $174,000, and a broader look at public administration and policy salaries shows just how far outside normal government compensation these numbers sit. The proposal's author treats that gap as a feature rather than a flaw, arguing that the only way to meaningfully redirect the attention of high-achieving individuals is to make the financial stakes proportionate to the decisions being made.

The Principal-Agent Problem at the Heart of the Design

For students and practitioners in MPA and MPP programs, this proposal is a textbook illustration of the principal-agent problem in democratic governance. Voters act as principals who want long-term fiscal sustainability, but they have limited tools to enforce that preference on legislators, the agents who control spending and revenue decisions. Elections occur every two or six years and rarely turn on a single budget variable. The surplus-linked pay model attempts to fill that gap by embedding a direct monetary signal into the decision calculus of every sitting member. Whether monetary incentives can substitute for, or complement, electoral accountability is precisely the kind of question that public policy consultants and academic researchers debate in policy design courses.

How the Bonus Pool Would Work

Under the surplus-linked pay proposal, congressional bonuses would follow a structured sequence from fiscal achievement to individual payout. The mechanism is designed to create a direct financial stake for legislators in long-term budget discipline, with payouts scaled by chamber size and years of service.

Historical Context: How Often Has the U.S. Run a Budget Surplus?

Understanding how rarely the federal government has finished a fiscal year in the black is essential for evaluating any proposal that uses a surplus as a trigger condition. The historical record, drawn from the Office of Management and Budget's summary of receipts, outlays, and surpluses or deficits, paints a striking picture.1

Five Surplus Years in Over Six Decades

Since 1960, the federal government has recorded an annual budget surplus in only five fiscal years: 1969, 1998, 1999, 2000, and 2001.1 The 1969 surplus was modest, roughly $3.2 billion. The four consecutive surplus years from 1998 through 2001 were far more substantial, peaking at approximately $236.4 billion in fiscal year 2000.1 That four-year window was driven by a convergence of factors that policy scholars rarely see aligned at the same time: rapid economic growth fueled by the technology boom, rising capital gains tax receipts, restrained discretionary spending following the 1997 Balanced Budget Act, and a declining defense budget in the post-Cold War period. Since fiscal year 2001, no annual surplus has occurred.1

Annual Surpluses Versus Monthly Surpluses

It is worth distinguishing between annual and monthly budget outcomes. Even in years when the government runs a large annual deficit, the Treasury frequently posts monthly surpluses, particularly in April when individual income tax payments flood in. A proposal that defines its trigger using an annual surplus creates a vastly different incentive than one that relies on monthly or quarterly measures. The annual metric is harder to game or cherry-pick, but it also means the incentive fires far less frequently. How the trigger condition is defined in any surplus-linked pay scheme would materially shape both its behavioral impact and its vulnerability to timing manipulation.

What Produces a Surplus?

At its core, a surplus occurs when federal revenues exceed outlays. Historically, achieving that balance has required both strong economic growth (which lifts tax receipts through higher incomes, corporate profits, and capital gains) and restrained spending growth. Neither condition alone has proven sufficient. Revenue surges during economic expansions have repeatedly been absorbed by spending increases, while spending cuts during weak economies tend to reduce revenue through slower growth, a dynamic fiscal policy careers in public administration students know as the "automatic stabilizer" problem.

Implications for the Proposal

The rarity of surpluses raises a fundamental design question. If the incentive trigger has fired only five times in more than sixty years, can it plausibly motivate sustained behavioral change among legislators? From a behavioral economics perspective, rewards that are extremely uncertain and far in the future tend to have weak motivational power. Policymakers and MPA/MPP students should consider whether the proposal functions more as an aspirational signal about fiscal values than as a realistic performance-pay mechanism. A trigger that almost never activates may not reshape incentives so much as underscore just how structurally difficult surplus budgeting has become in an era of mandatory spending growth, rising interest obligations, and deep partisan disagreement over both revenue and expenditure priorities.

The U.S. has run an annual budget surplus in only four of the last 60 years (1998 to 2001), meaning the proposed bonus pool would have been triggered less than 7 percent of the time. Behavioral economics suggests that rewards this infrequent may be too remote to reliably shape day-to-day legislative behavior.

Constitutional and Legal Constraints on Performance-Based Congressional Pay

The 27th Amendment creates a formidable legal barrier to any performance-based congressional compensation system, including bonuses tied to budget surpluses. Ratified in 1992,1 the amendment states that "No law, varying the compensation for the services of the Senators and Representatives, shall take effect, until an election of Representatives shall have intervened."2 While this language clearly prohibits immediate pay changes, the core legal question is whether a conditional bonus triggered by an external fiscal outcome constitutes "varying the compensation" in a way the amendment forbids.

The COLA Precedent and Its Limits

The only significant judicial interpretation of the 27th Amendment came in Boehner v. Anderson (30 F.3d 156, 1994), which upheld the automatic cost-of-living adjustment (COLA) mechanism for congressional pay.3 The D.C. Circuit found the COLA constitutional because the first adjustment took effect only after an intervening House election. However, a budget-surplus bonus differs fundamentally from a COLA. The COLA is a predictable, inflation-indexed adjustment applied uniformly regardless of legislative performance. A performance-based bonus, by contrast, introduces variability directly tied to congressional fiscal decisions, raising the question of whether each surplus-triggered payout represents a new "law varying the compensation" that must await an election.3

Scholarly consensus interprets "varying the compensation" broadly.4 Legal commentators generally argue that the 27th Amendment captures any mechanism that changes the amount lawmakers receive for their services, whether through base salary adjustments, bonuses, or conditional incentives. Under this reading, a surplus-linked bonus enacted in one Congress and paying out before the next House election would violate the amendment's core prohibition. Notably, scholars also confirm that the amendment's scope covers both pay increases and decreases, leaving no obvious workaround through reduced base salaries offset by bonuses.4

Structural and Separation-of-Powers Concerns

Article I, Section 6 of the Constitution establishes that members of Congress "shall receive a Compensation for their Services, to be ascertained by Law." Conditioning that compensation on executive-branch fiscal data (budget outcomes reported by the Office of Management and Budget and the Treasury Department) raises separation-of-powers questions. If congressional pay depends on executive-branch calculations, does that create an improper dependency or give the executive branch leverage over the legislative branch? While federal budget numbers are ostensibly objective, disputes over accounting methods, baseline assumptions, and classification of revenue and spending are common, potentially injecting conflict into what should be a purely legislative compensation decision.

Another case, Schaffer v. Clinton, challenged aspects of congressional pay but was dismissed on standing grounds by the Tenth Circuit,3 leaving no Supreme Court precedent directly interpreting the 27th Amendment.2 Without authoritative case law, any surplus-linked bonus statute would face immediate constitutional challenge and an uncertain judicial outcome.

Implementation Pathways and Barriers

Two pathways could potentially permit performance-based congressional pay. First, a constitutional amendment explicitly authorizing conditional compensation would remove all 27th Amendment ambiguity, but the amendment process is arduous and politically unlikely. Second, extremely careful statutory drafting might limit the bonus to members elected after the law's passage, applying only to future Congresses and ensuring an intervening election before any payout.5 Even this approach carries risk: if a bonus pool is created by statute in 2026 but pays out in 2027 to members who took office in January 2025, has the compensation been "varied" without an intervening election for those specific individuals?

The constitutional barrier is the proposal's highest hurdle. Without either a constitutional amendment or a Supreme Court willing to adopt a narrow reading of "varying the compensation," any surplus-linked bonus system faces a strong likelihood of judicial invalidation. For public administration and policy students and practitioners, this illustrates a fundamental tension in incentive design: the most direct performance mechanisms often collide with structural safeguards intended to preserve legislative independence and accountability to voters rather than to external metrics.

Precedents: The No Budget No Pay Act and Other Conditional-Pay Proposals

Congress has flirted with conditional pay before, and the history of those experiments offers a useful baseline for evaluating whether linking salaries to budget surpluses would actually change behavior.

The No Budget, No Pay Act of 2013

The best-known example is H.R. 325, enacted on February 4, 2013, as Public Law 113-3.1 Sponsored by Rep. Dave Camp (R-MI), the bill passed as part of a broader debt ceiling deal that suspended the debt limit through May 18, 2013.2 Its core mechanism was an escrow arrangement: if either chamber failed to adopt a fiscal year 2014 budget resolution by April 15, 2013, member salaries would be deposited into an escrow account rather than paid out directly. The money would be released only once the chamber passed a budget or the 113th Congress ended, whichever came first.2

The architects of the law were careful about one constitutional wrinkle. The Twenty-Seventh Amendment bars any law varying congressional compensation from taking effect until an intervening election has occurred. The escrow approach sidestepped this by delaying payment timing rather than reducing nominal compensation, a distinction that legal scholars at UC Davis School of Law examined in some depth at the time.3

In practice, the law had no bite. The Senate passed a budget resolution before the April 15 deadline, meaning no pay was ever placed in escrow.4 The measure served more as a public signal than a structural reform.

Earlier and Later Variations

The 2013 law had predecessors. Rep. Jim Cooper introduced a version in 2012 that would have denied pay outright if a budget was not enacted by October 1 of that year, a harder penalty and one that raised starker constitutional questions.1 More recently, Rep. Rob Wittman introduced H.R. 225 in the 118th Congress under the same "No Budget, No Pay" banner, again proposing an escrow hold until a budget passed or the session ended.4

These bills share a common architecture: a process-based trigger. Pay is conditioned on completing a procedural step, passing a budget resolution, rather than on achieving any measurable fiscal outcome.

Process Triggers Versus Outcome Triggers

This distinction matters enormously for public policy making. A process trigger rewards compliance with a deadline. An outcome trigger, such as the surplus-linked proposal circulating at fixtheincentives.com, rewards a result. The difference shifts both the difficulty and the behavioral logic considerably. Congress can pass a budget that projects surpluses it never delivers; it cannot, by definition, claim a surplus that arithmetic does not confirm.

At the same time, the track record of process-based conditional pay is not encouraging. The 2013 law generated little lasting change in how Congress approached the budget calendar, and subsequent iterations have stalled without floor votes.4 That pattern suggests the obstacle may be less about incentives than about the underlying political economy: deficits tend to be popular in the short run because they defer costs, and no pay structure, however clever, fully resolves that dynamic. Whether an outcome-based model would produce different results is genuinely uncertain, and honest policy analysis requires acknowledging that uncertainty upfront.

Questions to Ask Yourself

If the No Budget No Pay Act failed to change legislative behavior despite immediate pay consequences, why would a surplus-linked bonus triggered once every 15+ years succeed?

The rarity of surpluses may make the incentive too distant to influence day-to-day votes. Behavioral economics shows that immediate consequences shape decisions far more effectively than infrequent, uncertain rewards decades in the future.

Is the real barrier to fiscal discipline misaligned incentives in Congress, or is it that voters consistently reward deficit spending on popular programs?

Legislators respond to constituent demands. If voters punish spending cuts and reward new benefits regardless of cost, no pay structure will overcome the electoral pressure to run deficits and avoid tough tradeoffs.

Could bonus pay create perverse incentives to slash critical investments or shift costs off-budget to engineer a technical surplus?

When lawmakers stand to gain millions personally, the risk of accounting gimmicks, deferred maintenance, and underinvestment in infrastructure or research grows. The policy goal should be sustainable fiscal health, not a one-year accounting win.

Incentive Design Analysis: Pros, Cons, and Perverse Effects

Evaluating this proposal requires the lens of behavioral public choice theory, which examines how institutional incentives shape the decisions of rational, self-interested actors within government. The core tension is straightforward: when the potential reward is enormous but any single legislator's causal contribution to a budget surplus is negligible, the incentive structure may warp priorities without producing the intended fiscal discipline. For students and practitioners of public administration, this case study illustrates why incentive design in governance demands far more nuance than in private sector compensation.

Pros

Aligns legislators' personal financial interests with long-term fiscal sustainability, creating a direct stake in balanced budgets.

The 10-year credit payout structure encourages sustained fiscal discipline rather than short-term budget manipulation before elections.

Introduces a market-like feedback mechanism into governance, rewarding measurable outcomes instead of symbolic legislative activity.

Could attract fiscally minded candidates to congressional races by making responsible budgeting a personally lucrative endeavor.

Shifts the political calculus so that deficit spending carries an opportunity cost legislators can feel in their own compensation.

Cons

May incentivize accounting gimmicks such as off-budget spending, asset sales, or trust fund raids that manufacture paper surpluses without real fiscal improvement.

Could encourage pro-cyclical austerity during recessions, pressuring Congress to cut spending precisely when countercyclical investment is most needed.

Creates a severe collective action problem: each member's marginal impact on total federal revenue and spending is negligible, weakening the motivational link.

Bonus amounts ranging from $1.5 million to $30 million per year could dramatically worsen public distrust of Congress and perceptions of legislative self-dealing.

Rewards correlated with macroeconomic conditions outside congressional control (e.g., tax revenue driven by growth cycles) may produce windfalls unrelated to legislative merit.

Risk of perverse prioritization, where legislators focus narrowly on surplus generation at the expense of critical investments in infrastructure, defense, or social programs.

Comparative Practices: State Legislatures and International Models

No legislature anywhere in the developed world currently ties its members' base pay or bonuses directly to fiscal surplus performance. That absence is itself the most important data point for evaluating the federal proposal: students assessing feasibility are looking at an idea with no operational precedent to study.

What U.S. States Actually Do

State legislative compensation follows three main patterns: salaries set by statute, salaries set by an independent compensation commission, or salaries pegged to other public-sector pay benchmarks.1 Roughly 19 states use a compensation commission model, and in places like Arizona and Nebraska any commission recommendation must go to voters for approval.2 Compensation packages typically combine an annual salary, a per diem for session days, and mileage reimbursement calculated at the federal rate.3

What none of these states do, as of 2024, is condition legislator pay on a balanced budget, a surplus, or any other fiscal outcome metric.3 The closest analogs are "no budget, no pay" proposals that surface periodically, including a Facebook-circulated idea suggesting lawmakers forfeit pay for every day a budget is late.4 These proposals punish procedural failure (missing a deadline) rather than reward substantive fiscal performance (running a surplus). The distinction matters: docking pay for tardiness is administratively simple and politically popular, while linking pay to surplus introduces measurement, timing, and gaming problems that no jurisdiction has tried to solve.

International and Executive-Branch Comparisons

Internationally, Singapore's ministerial salary framework is sometimes cited as a pay-for-performance model, but it applies to executive officeholders, not parliamentarians, and benchmarks salaries to top private-sector earners rather than to fiscal outcomes. Switzerland's debt brake constrains spending and borrowing through constitutional rules, but it does not touch legislator compensation.

This points to a broader pattern. Defining public policy goals is far easier than designing accountability mechanisms that hold collective legislative bodies to them. Pay-for-performance arrangements exist in executive and administrative contexts, where a single decision-maker or small team can be held accountable for measurable results. Legislatures are collective bodies of hundreds of members whose individual contributions to a fiscal outcome are essentially impossible to isolate. That structural feature, more than ideology, explains why legislative pay-for-performance remains theoretical.

For policy students, the takeaway is calibrated skepticism. The absence of precedent does not disqualify the proposal, but it does mean any adoption would be a genuine experiment, with no comparable case to draw lessons from.

Public Opinion: Do Americans Want Congressional Pay Tied to Results?

While no major national poll has directly asked whether congressional pay should be linked to budget surpluses, several data points reveal a public deeply skeptical of Congress and broadly supportive of accountability measures. The gap between overwhelming public demand for performance accountability and the constitutional and political barriers to enacting such reforms remains one of the central tensions in this policy debate.

Implications for Public Administration Students and Practitioners

For graduate students in public administration and public policy degrees, a proposal to tie congressional pay to federal budget surpluses is not just a political curiosity. It is a working case study in how analysts diagnose dysfunction in democratic institutions and design rules intended to correct it. Whether or not the specific mechanism ever reaches a committee markup, the underlying question (how do you align the personal interests of elected officials with long-term fiscal stewardship?) sits at the center of the MPA and MPP curriculum.

Where This Fits in the Curriculum

The proposal touches at least three required course areas. In public finance, it forces a conversation about why structural deficits persist across administrations of both parties. In organizational behavior and human resource management, it raises the same incentive-design questions that arise when agencies experiment with performance pay. In policy analysis, it offers a clean example of a proposed intervention whose theory of change, side effects, and feasibility can all be stress-tested using standard tools.

Analytical Frameworks Worth Applying

Students evaluating this idea should not stop at intuition. Several frameworks taught in graduate programs apply directly:

Ostrom's Institutional Analysis and Development framework: useful for mapping the rules-in-use, actors, and payoffs that produce current budget outcomes, and for asking which rules a pay rule would actually change.

Wilson's typology of bureaucratic and political incentives: clarifies whether legislators behave more like coping, craft, procedural, or production actors, and whether outputs (a budget vote) or outcomes (a surplus) are observable enough to reward.

Buchanan and Tullock's public choice theory: predicts how rational legislators would respond to a surplus-linked bonus, including the temptation to manipulate accounting definitions or shift costs off-budget.

Practitioner Takeaways

For working analysts and aspiring agency leaders, the more durable lesson is methodological. Accountability mechanisms for elected officials, from term limits to PAYGO to balanced budget requirements, all share the same design problem: defining a measurable result, attributing it to specific actors, and avoiding perverse responses. Honest assessment suggests this proposal is more valuable as a thought experiment that clarifies what genuine fiscal incentive alignment would require than as a viable legislative vehicle. That clarification, however, is exactly the kind of analytic work public administration journals document and the public sector needs more of.

Frequently Asked Questions About Congressional Pay and Budget Surpluses

The intersection of congressional compensation and federal fiscal outcomes raises questions that span constitutional law, budgetary history, and incentive theory. Below are answers to the most common questions students, practitioners, and policy observers raise about this topic.

How would the federal government create a budget surplus?

A surplus occurs when total federal revenues exceed total outlays in a given fiscal year. Achieving one requires some combination of higher tax collections, reduced spending, or robust economic growth that boosts receipts. With federal debt exceeding $37 trillion and interest payments consuming roughly 14% of spending as of 2026, a surplus would likely demand significant structural changes to both revenue policy and mandatory spending programs such as Social Security and Medicare.

Are congressmen paid a salary out of the Treasury of the United States?

Yes. Article I, Section 6 of the Constitution provides that senators and representatives "shall receive a Compensation for their Services, to be ascertained by Law, and paid out of the Treasury of the United States." Since 2009, the base salary for most members of Congress has been $174,000 per year. Leadership positions, including the Speaker of the House and the president pro tempore of the Senate, receive higher compensation.

Does the 27th Amendment prevent tying congressional pay to budget outcomes?

The 27th Amendment prohibits any law varying congressional compensation from taking effect until after the next election of representatives. A surplus-linked bonus structure would need careful design so that payouts are triggered only after an intervening election. Whether a performance bonus qualifies as a "varying" of compensation would almost certainly face legal challenge. Proponents argue structuring the benefit as a deferred incentive could satisfy the amendment's requirements, though courts have not ruled on this specific question.

What is the No Budget No Pay Act and has it ever been enacted?

The No Budget, No Pay Act of 2013 temporarily suspended congressional pay when either chamber failed to pass a budget resolution. It was enacted once and applied to a brief window in early 2013. While the concept demonstrated public appetite for accountability-based pay, it functioned more as a political pressure tool than a lasting fiscal incentive. Several subsequent versions have been proposed but none has been signed into law since.

How often has the U.S. federal government run an annual budget surplus?

Annual surpluses have been exceptionally rare in modern history. The most recent stretch occurred during fiscal years 1998 through 2001, driven by strong economic growth, capital gains revenue, and spending restraint following the 1997 Balanced Budget Act. Before that, the last surplus was in 1969. Over the past century, deficits have been the norm, making any proposal that rewards surpluses a long-horizon incentive rather than a near-term compensation mechanism.

Would tying congressional pay to surpluses create perverse spending incentives?

Critics warn of several risks. Lawmakers might pursue short-term budget gimmicks, such as shifting spending off-budget or accelerating revenue collection, to manufacture artificial surpluses. They could also cut politically vulnerable programs while protecting those that benefit powerful constituencies. Aggressive austerity to trigger bonuses might harm economic stability during recessions. Careful incentive design, including independent verification of fiscal outcomes and protections against accounting manipulation, would be essential to mitigate these effects.