Public Housing Policy: Understanding the Challenges and What Reform Could Look Like

How chronic underfunding, stock loss, and shifting demographics are reshaping one of America's core affordable housing programs — and what public administrators need to know.

By Max SheltonReviewed by PAP Editoral TeamUpdated July 21, 202625+ min read

What you’ll learn in this article…

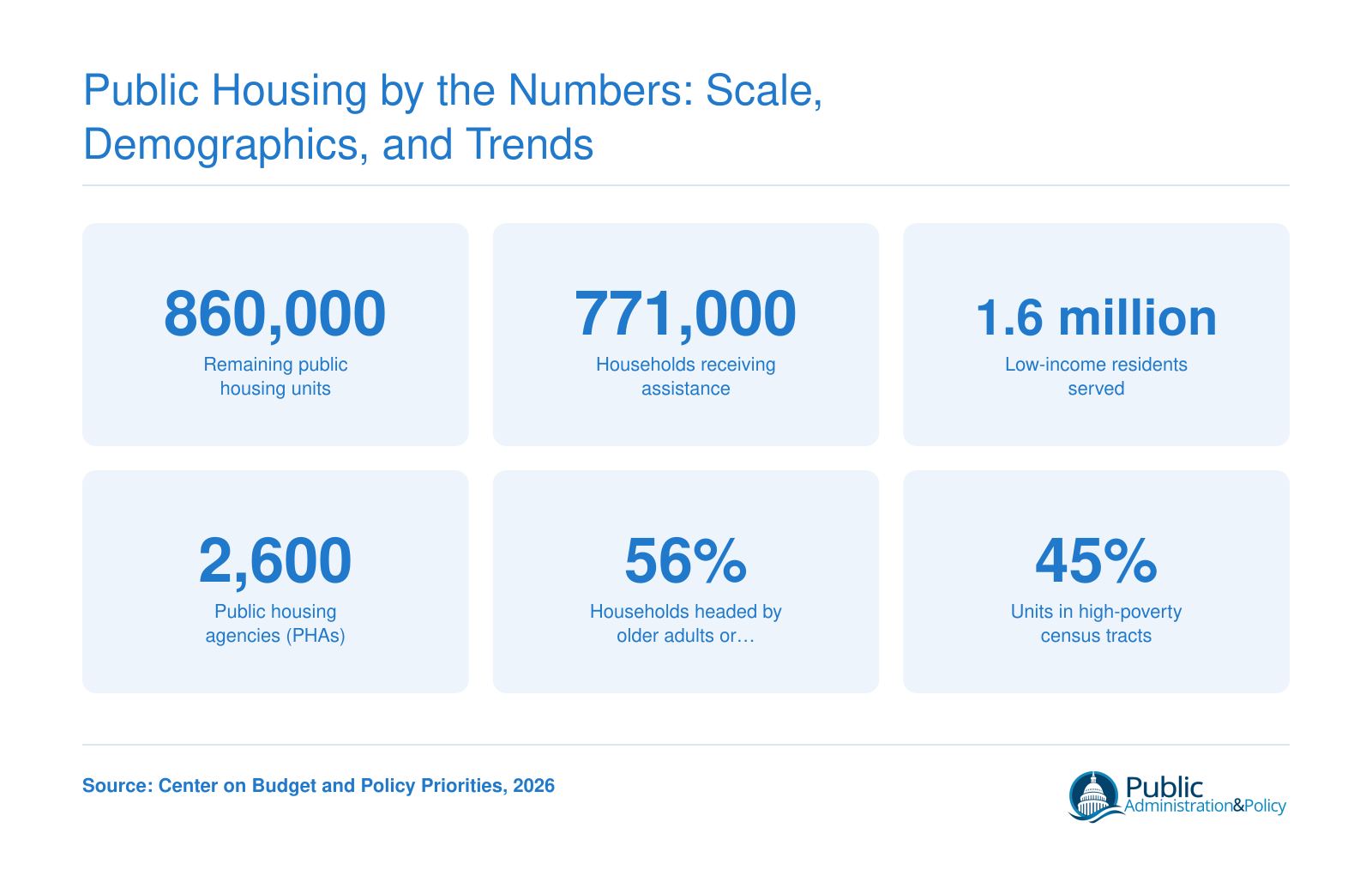

Since 1996, the U.S. has built no new public housing while the stock declined from 1.3 million to 860,000 units.

HUD’s public housing capital repair backlog exceeds $70 billion and will reach $169 billion over a decade.

Nearly 200,000 public housing units have been converted to Section 8 vouchers under the RAD program since 2012.

Forty-five percent of public housing homes are in high-poverty areas, reflecting decades of segregationist siting policies.

The decision between preserving aging public housing stock and shifting resources to tenant-based vouchers has reshaped American housing policy over three decades. Public housing has shed over 400,000 units since the mid-1990s, from 1.3 million to just 860,000 in 2026, even as 1.6 million people still rely on the program.1

Chronic underfunding of the Public Housing Operating and Capital Funds has left a repair backlog exceeding $70 billion, while nearly half of units sit in high-poverty neighborhoods. The Rental Assistance Demonstration program has converted nearly 200,000 units to Section 8, further blurring the line between project-based and voucher-based assistance.1

These dynamics place public housing agencies at the center of a difficult balancing act: preserving what remains while meeting the needs of an increasingly elderly and disabled resident population.

Public Housing by the Numbers: Scale, Demographics, and Trends

Public housing has undergone a dramatic transformation over the past three decades. No new units have been built since the mid-1990s, and the total stock has shrunk by over one-third even as the need for deeply affordable housing continues to grow. The population served has shifted, with a majority of households now headed by older adults or people with disabilities, and nearly half of all units remain clustered in high-poverty neighborhoods.

Core Challenges Facing Public Housing Today

Public housing in the United States confronts a web of interconnected problems that threaten its viability as a safety net for millions. The challenges are not isolated; they stem from decades of federal policy choices that have starved the program of resources while failing to address its structural flaws. This section unpacks five core areas of concern that policymakers and public administrators must grapple with.

Chronic Federal Underfunding

The single most consequential challenge is the persistent underfunding of the Public Housing Operating Fund and Capital Fund. Over 19 of the last 25 years, Congress has failed to fully fund these accounts according to need, leaving housing authorities to operate with less than what it costs to maintain decent conditions.1 This consistent shortfall forces trade-offs between immediate repairs and long-term capital improvements. For the 1.6 million low-income residents and 771,000 households assisted, the result is a growing backlog of maintenance issues that compromises health, safety, and quality of life. Without adequate annual appropriations, the program cannot keep pace with rising costs or aging infrastructure.

The Capital Repair Backlog

Years of underfunding have produced a capital repair backlog that HUD estimates runs well into the tens of billions of dollars nationwide. Building systems including roofs, plumbing, elevators, and heating are well past their useful lives in many developments. Public housing units have declined from 1.3 million in the mid-1990s to roughly 860,000 by 2026, in part because severely deteriorated properties become too expensive to rehabilitate.1 When agencies cannot afford comprehensive modernization, they often resort to demolishing units rather than letting them fall into dangerous disrepair, further shrinking the stock.

Accelerating Unit Loss

The loss of public housing units is not simply a function of deterioration. Since the mid-1990s, no federal funds have been appropriated to construct additional public housing, and no replacement mandate exists for demolished homes. The Rental Assistance Demonstration program, discussed in the next section, has converted nearly 200,000 public housing units to Section 8 contracts since 2012, with authorization for up to 455,000 conversions.1 While this preserves affordability in the short term, it permanently removes units from the public housing inventory and shifts their governance and tenant protections into a voucher-based framework. The net effect is a steadily shrinking public housing stock that cannot meet demand.

Poverty Concentration and Fair Housing Failures

Where remaining public housing is located matters enormously. As of 2020, 45 percent of public housing homes were in census tracts where at least 30 percent of residents live below the poverty line.1 This concentration of high-poverty housing results from decades of discriminatory siting decisions, often placing developments in segregated, disinvested neighborhoods, and from fair housing enforcement that has been inconsistent at best. Urban planning and public policy tools have long recognized that neighborhood context shapes life outcomes, yet these lessons have rarely been applied consistently in public housing siting. For residents, this means limited access to high-performing schools, employment opportunities, transit, and safe environments, undercutting the program's mission to provide a platform for upward mobility.

PHA Governance and Capacity Gaps

The roughly 2,600 public housing agencies that administer the program vary dramatically in scale and capability. Large metropolitan authorities manage complex portfolios of thousands of units and can often attract skilled staff and leverage financing tools. In contrast, many smaller agencies oversee fewer than 100 units with minimal staffing, outdated technology, and limited expertise in financial management or property redevelopment. This uneven capacity leads to wide disparities in service quality, waitlist management, and physical upkeep. For residents, the experience of public housing can look very different depending on which agency holds the keys, raising concerns about equity and administrative accountability.

These challenges are not independent. Chronic underfunding accelerates physical deterioration; deteriorating units become candidates for demolition or conversion; the remaining stock shrinks and often concentrates in high-poverty neighborhoods; and agencies with the least capacity are least equipped to reverse the cycle. Reform proposals must address this interconnected system rather than treating symptoms in isolation.

The $70+ Billion Question: Understanding the Capital Repair Backlog

The national capital repair backlog for public housing currently exceeds $70 billion, according to HUD's latest assessments, with a 2025 ten-year preservation roadmap projecting $169.1 billion in needs over the next decade, roughly $188,000 per unit.1 For context, the last detailed HUD capital needs study in 2010 placed the backlog at $25.6 billion, with annual ongoing capital requirements at $3.4 billion.2 The gap between available funding and accumulated need has only widened since then.

A Dual-Funding System Stretched Past Its Limits

Public housing relies on two distinct federal funding streams, both of which have systematically fallen short. The Public Housing Operating Fund covers day-to-day expenses like utilities, routine maintenance, and staff salaries. The Capital Fund is supposed to handle major repairs, modernization, and accessibility upgrades. Yet over the past 25 years, Congress has fully funded these accounts in only six budget cycles. The remaining 19 years saw prorated allocations that failed to keep pace with rising costs and aging infrastructure.3

Because the Capital Fund is discretionary and competes with other domestic priorities, shortfalls compound annually. When a roof repair is deferred at $50,000, water intrusion can escalate the need into a full roof replacement and structural remediation costing $500,000 or more. This dynamic turns a maintenance backlog into a rolling financial crisis that no government program manager can budget their way out of.

From Deferred Maintenance to Structural Crisis

On the ground, the capital backlog translates into leaking plumbing, failing HVAC systems, broken elevators, outdated electrical panels, and widespread environmental hazards. Lead paint abatement and mold remediation are among the most expensive line items, especially in properties built before 1978. A single elevator modernization can exceed $200,000; a boiler replacement can run several million dollars for a large high-rise. When hundreds of units require multiple interventions simultaneously, per-unit costs quickly outstrip annual capital grants, which often average only a few thousand dollars per unit.

The downward spiral is measurable. In 2010, the per-unit backlog stood at $23,365.2 By 2025, the per-unit preservation need had ballooned to $188,090 over ten years.1 This reflects not only inflation but the compounding effect of neglected systems: a slow leak eventually destroys walls, floors, and neighboring units, multiplying the scope of work.

When Repair Costs Exceed Replacement Value

One perverse outcome of the chronic backlog is that housing authorities sometimes conclude rehabilitation is no longer cost-effective. When the capital repair estimate approaches or exceeds the cost of demolition and tenant relocation, the asset is deemed beyond preservation. Urban policy planners and housing administrators then pursue disposition or demolition, often converting the land to mixed-income redevelopment or simply removing the units from inventory. This pattern has accelerated the net loss of public housing stock, from 1.3 million units in the mid-1990s to 860,000 in 2026, even as waiting lists grow. The capital backlog thus becomes a direct driver of unit loss, concentrating poverty in remaining properties that face the same funding constraints.

Deferring maintenance doesn't just postpone costs, it multiplies them. A small roof patch left unfixed can escalate into a full replacement, turning a five-thousand-dollar job into a fifty-thousand-dollar crisis. Each year of underinvestment compounds; what could be solved with routine repair soon demands major capital projects, straining already tight public housing budgets.

RAD Conversions and the Shift to Section 8

The Rental Assistance Demonstration program has become the dominant federal strategy for preserving aging public housing, but its legacy is a fundamental redefinition of what public housing means.

What Is RAD and How Does It Work?

The Rental Assistance Demonstration, created in 2012, permits public housing agencies to convert their public housing units to long-term, project-based Section 8 contracts. Instead of relying on the chronically underfunded Public Housing Capital Fund for major repairs, PHAs leverage the Section 8 subsidy stream, which is more predictable and can support private debt and Low-Income Housing Tax Credit equity. The conversion unlocks billions of dollars in private financing that the traditional public housing model cannot access, allowing for immediate rehabilitation or redevelopment of distressed properties.

Scale and Reach of the Transformation

Since its inception, nearly 200,000 units have been converted under RAD, and HUD is authorized to permit up to 455,000 total conversions.1 This shift represents a substantial portion of the nation's remaining public housing inventory, which has already declined from 1.3 million units in the mid-1990s to about 860,000 in 2026. For many PHAs, RAD is the only viable path to recapitalize properties that would otherwise face demolition or severe deterioration, especially given that no new public housing units have been funded since the mid-1990s.

Why PHAs Choose Conversion

The administrative logic is clear: RAD provides access to financing tools that the Capital Fund cannot match. With tax credits and private debt, PHAs can address the staggering capital repair backlog estimated at over $70 billion nationally. The Section 8 contract also offers a more stable operating subsidy, reducing the year-to-year uncertainty of congressional appropriations. For residents, the up-front renovation improves living conditions dramatically, and long-term affordability protections are written into the contracts, typically requiring rents to remain at 30 percent of income.

Concerns and Administrative Hurdles

Conversion carries significant tensions. Once a unit is moved out of the public housing program, it is no longer technically public housing, and the property is governed by a different set of federal rules. Critics argue this erodes long-term public control, as the underlying mortgage and ownership structures can become complex mixed-finance arrangements involving private developers and investors. While resident protections are intended, advocates raise concerns about whether permanent affordability guarantees can survive future financial pressures or ownership changes. Additionally, managing the transition is administratively intensive: PHAs must navigate intricate legal and financial structuring, temporary resident relocation, and ensuring that resident rights, such as the right to return and grievance procedures, are clearly maintained throughout redevelopment. These challenges require deep expertise in public administration salary expectations and negotiation power, public finance, and housing law, often stretching the capacity of smaller housing authorities.

Public Housing Vs. Vouchers Vs. LIHTC: How Resident Outcomes Compare

Voucher-assisted households are exposed to neighborhood poverty rates that are 5.2 percentage points lower than similar unassisted families, according to a 2022 systematic review.1 This finding captures a core dynamic in the debate over how to design federal housing assistance: different subsidy mechanisms produce different resident experiences.

Three Delivery Models, Three Resident Experiences

The United States relies on three major programs to subsidize rental housing for low-income households, each operating through a distinct delivery mechanism. Public housing consists of units owned and operated by local public housing agencies, tying assistance to the unit itself. Housing Choice Vouchers provide tenant-based subsidies that families can use in the private market, offering the flexibility to move. The Low-Income Housing Tax Credit (LIHTC) encourages private development of income-restricted units, typically project-based for a compliance period. These structural differences shape everything from neighborhood access to tenant stability, making outcome comparisons both urgent and difficult.

Voucher Outcomes: A Building Evidence Base

The most robust research to date focuses on Housing Choice Vouchers, often comparing families who receive a voucher to those still on waiting lists. Evidence from The Community Guide and a 2022 review in Health Affairs points to several measurable gains:1

- Health conditions: 4.0 percentage point decrease in adults reporting health problems.

- Unmet medical needs: 4.1 percentage point decline.

- Employment rate: 3.0 percentage point increase.

- Income: 20.6 percent higher earnings.

- College attendance: 3.4 percentage point boost.

- Poverty: 6.7 percentage point reduction in households below the poverty line.

- Neighborhood poverty exposure: 5.2 percentage points lower.

These improvements align with the core mechanism of vouchers: enabling families to move to lower-poverty neighborhoods with better schools and job opportunities. Yet health outcomes are mixed. One study found that 50 percent of voucher households had hypertension,2 underscoring how pre-existing health burdens persist even with housing assistance.

The Mobility-Stability Trade-Off

Project-based subsidies like public housing and LIHTC anchor families in place, which can preserve community ties and simplify service delivery. Vouchers, by contrast, trade some of that stability for the chance to choose a higher-opportunity location. Public policy and urban planning research suggests that this trade-off matters: voucher recipients who move to lower-poverty areas show larger gains in health and economic outcomes. For older adults and people with disabilities, however, the forced mobility of vouchers can strain caregiving networks, a concern as 56 percent of public housing households were headed by such individuals in 2024.

Why Direct Comparisons Remain Sparse

Rigorous apples-to-apples comparisons across all three programs are hindered by selection effects: voucher recipients often differ in motivation and resources from those who remain in project-based units. Regional variation in housing markets further confounds the picture. LIHTC outcomes, in particular, receive less empirical attention, partly because data linking tenant outcomes to specific tax-credit properties is less accessible. Policymakers must therefore weigh a nuanced body of evidence rather than a single clear ranking.

Questions to Ask Yourself

If your agency administers both public housing and vouchers, how do you weigh the cost of maintaining deteriorating units against the flexibility and uncertainty of voucher portability for your residents?

Asset-based aid locks in deeply affordable units but carries escalating capital costs, while vouchers offer mobility but depend on landlord participation and market rent levels, forcing agencies to balance fiscal stewardship with resident autonomy.

What does preservation actually mean when the physical stock is crumbling, and at what point does reinvestment become economically irrational?

With a $70 billion repair backlog, agencies must define preservation not just as building longevity but as sustaining habitable, healthy housing; pouring resources into structurally obsolete properties may undermine the program's long-term viability.

As more units convert under RAD to Section 8 project-based assistance, how does your agency mitigate the risk of displacing elderly or disabled residents from their established communities?

Relocation can sever ties to healthcare, social networks, and jobs; administrators must weigh the urgency of rehabilitation against the human cost of uprooting vulnerable households, especially when replacement units are scarce in opportunity-rich areas.

How should public housing authorities prioritize capital improvements when funding covers only a small fraction of needs, and what equity criteria guide decisions to preserve, convert, or demolish?

Scarce resources and aging infrastructure demand transparent triage that considers resident health, energy efficiency, and geographic equity, all while navigating political pressures and the legal mandate to affirmatively further fair housing.

Racial Equity, Fair Housing, and the Geography of Poverty Concentration

The concentration of public housing in high-poverty, racially segregated neighborhoods is not an unfortunate byproduct of market forces; it is the direct result of decades of deliberate government policy. From the inception of the public housing program, local officials used site selection, zoning, and racially restrictive covenants to isolate Black families in disinvested areas, while creating separate, higher-quality developments for white households. That legacy persists in the geography of need today.

The 45% High-Poverty Reality

As of 2020, 45 percent of public housing homes are located in census tracts where at least 30 percent of residents live below the poverty line.1 These neighborhoods typically also have weaker schools, fewer jobs, and worse health outcomes. For the 1.6 million low-income people who rely on public housing, 56 percent of whom are households headed by older adults or people with disabilities, place means more than shelter; it shapes life trajectories.

How Public Housing Segregation Compares to Vouchers and LIHTC

The demographics of public housing differ notably from other federal rental assistance programs. Black and Hispanic households make up a larger share of public housing residents than they do of Housing Choice Voucher participants or tenants in Low-Income Housing Tax Credit (LIHTC) properties. Voucher holders, while still often clustered in lower-opportunity neighborhoods, have somewhat more mobility, though landlord discrimination and tight rental markets limit that potential. LIHTC developments, meanwhile, tend to be sited in slightly lower-poverty tracts but still replicate patterns of racial concentration. These disparities raise fundamental questions for the Affirmatively Furthering Fair Housing (AFFH) mandate, which requires HUD and its grantees to take meaningful actions to overcome historic segregation. How urban planning improves quality of life is directly relevant here, as siting decisions and neighborhood investment strategies sit at the intersection of land use, equity, and public policy.

Place-Based Investment versus Mobility: The Fair Housing Policy Fork

Public housing policy faces a persistent tension: invest heavily in improving the neighborhoods where public housing already exists, or help residents move to areas with greater opportunity. Place-based strategies, such as the Rental Assistance Demonstration (RAD) and Choice Neighborhoods, aim to revitalize existing developments and surrounding communities, but risk gentrification and displacement. Mobility approaches, like enhanced voucher counseling and source-of-income protection laws, seek to open doors to high-opportunity suburbs and cities, yet they can inadvertently drain social capital from legacy communities. Neither approach alone is sufficient.

AFFH Enforcement in a Shifting Regulatory Landscape

The ability of public housing agencies (PHAs) to advance racial equity depends significantly on federal fair housing enforcement. The AFFH rule, first strengthened in 2015 and then substantially weakened in 2020, has been in a state of uncertainty. As of mid-2026, HUD has signaled a return to more robust oversight, but PHAs report limited staff capacity to complete equity assessments or overhaul siting practices. Many agencies are piloting tools like opportunity mapping and racial equity impact analyses, yet sustained funding for such efforts remains elusive. For public administrators, the challenge is to embed fair housing principles into everyday operations despite inconsistent federal support.

Leading Reform Proposals for the Mid-2020S

What federal policy changes are actually on the table for public housing in the mid-2020s?

Faircloth Amendment Repeal: The Threshold for Growth

The Faircloth Amendment, which caps public housing units at pre-1999 levels, continues to block new construction. In 2026, several bills (including H.R. 659 and S. 2234) sought repeal, but none have passed.1 Advocates from the National Low Income Housing Coalition argue that lifting this cap is essential to reverse decades of unit loss.2 Without repeal, even fully funded capital budgets cannot restore the housing stock that has disappeared since the mid-1990s.

Capital Investment: A $70 Billion Question

The accumulated repair backlog exceeds $70 billion, yet no dedicated appropriation has emerged. The Housing for the 21st Century Act (H.R. 6644), which passed the House 390-9 in 2026, lifts the RAD cap and streamlines NEPA reviews but does not provide direct capital infusions.3 Similarly, the Senate Banking Committee's unanimous passage of the ROAD to Housing Act (S. 2651) offers RAD expansion and regulatory flexibilities.3 The One Big Beautiful Bill Act (P.L. 119-21), enacted in 2026, expanded LIHTC allocations, providing an indirect boost to affordable housing finance.3 The National Infrastructure Bank Act and the Build Housing With Care Act remain only proposed, leaving the large-scale capital infusion that advocates demand still out of reach.

Rent Reform: Rethinking the 30 Percent Model

Most tenants pay 30 percent of adjusted income, with a $50 minimum rent permitted. Public policy making shapes how alternatives such as stepped rents, flat rents, or earned income disregards are evaluated, yet no major federal rent reform bill is near passage in 2026.3 HUD has permitted some local flexibility, but systemic change remains elusive, forcing agencies to navigate patchwork policies that can disincentivize income gains.

Resilient Retrofits and Green Mandates

HUD's mid-2020s regulatory push includes adjustments to Build America Buy America (BABA) requirements, opening the door for modern materials that support energy efficiency.3 While no stand-alone climate bill targets public housing, several proposals tie capital grants to decarbonization and climate adaptation. States and local agencies increasingly pilot green retrofit programs, but federal policy lacks a coordinated mandate for aging properties.

Social Housing: An Emerging Model

Alternative models are gaining traction. Montgomery County, Maryland's Housing Opportunities Commission (HOC) exemplifies a social housing development authority that operates outside traditional public housing and private-developer constraints. Community land trusts and mixed-income redevelopment schemes also appear in local pilots. However, no federal social housing authority has been enacted,3 leaving these experiments without national-scale support or dedicated financing.

International Models: What Vienna, Singapore, and the Netherlands Can Teach U.S. Policymakers

While the U.S. public housing system faces severe underfunding, several countries offer policy models that prioritize affordable housing as a long-term public good. These systems differ in scale, tenure, and funding, but they share design principles worth examining.

Vienna's Social Housing Model: Deep Affordability Through Public Investment

Vienna demonstrates that large-scale social rental housing can remain viable. The city maintains roughly 40-45% of its housing stock as social or subsidized units, largely municipally owned (23-25%) or managed by limited-profit associations.1 Funding relies on an earmarked wage tax, generating about $240 million annually, and a revolving loan fund, providing a stable, dedicated revenue stream independent of annual appropriations.2 With income eligibility up to 180% of area median income, the system avoids isolating only the poorest households; about 60% of the city's residents qualify.1 This broad eligibility creates a wide political constituency, shielding housing investments from budget cuts.

Singapore's Housing and Development Board: Homeownership as Central Policy

Singapore takes a different path, with the state-owned Housing and Development Board (HDB) providing housing for over 80% of the resident population. The model emphasizes homeownership through long-term (99-year) leases, with prices calibrated to household income. HDB receives government grants and borrows from the national reserves, but ongoing operations are largely self-funded through sales proceeds, property taxes, and commercial rents in HDB estates. Income ceilings keep luxury buyers out, yet the majority of citizens can purchase. This approach fosters a broad sense of asset ownership across income levels.

The Netherlands: A Hybrid of Social Rental and Guarantee Finance

The Dutch social housing sector accounts for roughly 30-35% of the total stock, managed by independent housing associations. These associations finance construction and maintenance through commercial loans backed by a state guarantee fund (the WSW), reducing borrowing costs. Rents are tied to unit quality and tenant income, and associations are required to serve low- and moderate-income households. In recent years, policy has shifted toward more targeted allocation, but the core funding model, leveraging public guarantees rather than annual appropriations, provides stability.

Lessons for U.S. Policymakers

Comparative study reveals actionable principles despite distinct political economies. First, broad eligibility, as seen in Vienna and Singapore, creates political durability. When housing programs serve the middle class as well as the poor, they command broader electoral support, insulating them from the chronic underfunding that plagues U.S. public housing. Second, cross-subsidy financing, where revenues from market-rate development or commercial rents supplement affordable units, can reduce reliance on unpredictable federal appropriations. Vienna's earmarked wage tax and Singapore's integrated estate commercial income demonstrate dedicated revenue streams. Third, mixed-income design at the neighborhood level, rather than concentrating the poorest households, can improve resident outcomes and reduce spatial inequity. Urban policy planners can adapt these mechanisms through fair-share zoning, housing trust funds, and expanding rental assistance that serves a wider income band.

Important caveats apply. European states have stronger social welfare traditions and often own substantial land, lowering development costs. Singapore's land-lease system is an extreme case of public landownership. Yet even within the U.S. federalist framework, these models offer a menu of fiscal and governance tools, revolving loan funds, state-level employer taxes, public land banks, that could revitalize the nation's affordable housing approach without requiring wholesale system change.

Vienna’s municipal government owns roughly 220,000 apartments, housing nearly one in four city residents, and has built social housing continuously since 1919. In contrast, the U.S. has not funded new public housing construction since the mid-1990s.

What This Means for Public Administration Professionals

Public housing policy is not a legacy program winding down; it is a live, complex arena where skilled public administrators are urgently needed to navigate trillion-dollar infrastructure needs, deeply interwoven equity mandates, and a rapidly evolving funding landscape.

New Skills for a Shifting Landscape

Today's practitioners must master at least four distinct skill sets that were peripheral a generation ago. First, mixed-finance deal structuring , particularly the layered capital stacks under the Rental Assistance Demonstration (RAD) , requires fluency in public-private partnerships, tax-credit syndication, and debt financing rarely taught in traditional public administration degrees curricula. Second, data-driven capital planning has become central as agencies must prioritize repairs across aging portfolios with limited funding, using asset management databases and predictive analytics to justify every dollar. Third, fair housing compliance now demands proactive, evidence-based strategies to desegregate opportunity neighborhoods, not just passive non-discrimination. Fourth, deep community engagement skills are essential: residents in public housing are disproportionately older adults and people with disabilities, and any reform must be co-designed with them rather than imposed.

The Leadership Succession Imperative

Just as the resident population is aging, so is the leadership of the 2,600 public housing authorities nationwide. Many executive directors and senior program managers entered the field during the last major construction wave in the 1970s and 80s and are now approaching retirement. Succession planning and talent pipeline development are critical needs, yet few graduate programs have explicit tracks in affordable housing management. MPA and MPP graduates who can combine policy analysis with operational execution, understanding both federal regulation and on-the-ground property management, will find themselves in high demand, not just at HUD but in city housing departments, state finance agencies, and mission-driven nonprofits. Careers in public administration span all of these sectors, and housing policy roles are among the fastest-growing areas of need.

A Career Arena, Not a Sunset Program

Students and mid-career professionals often mistakenly see public housing as a shrinking relic. In reality, the sector sits at the intersection of the country's most pressing public priorities: climate resilience retrofits for thousands of units, racial equity action plans, post-pandemic health and ventilation standards, and ongoing Congressional debates over the largest capital investment in affordable housing in decades. The professionals who step into these roles will shape whether public housing survives as a core safety-net institution or is permanently replaced by voucher-based models. That is not custodial work , it is high-stakes public governance.

Common Questions About Public Housing Policy

This FAQ addresses the most pressing questions about the current state of public housing in the United States. Drawing on recent data and policy analysis, the answers clarify challenges, funding structures, and leading reform ideas for policymakers and public administrators.

What are the main challenges of public housing in the United States?

Chronic federal underfunding has left many properties with deteriorating conditions and a substantial capital repair backlog. No new units have been built since the mid-1990s, while the stock shrank from 1.3 million to 860,000. Additionally, 45% of public housing homes are in high-poverty areas, and administrative complexity across 2,600 local agencies creates service delivery hurdles.

Why has the number of public housing units declined since the 1990s?

No federal funds have been provided for new public housing construction since the mid-1990s. Operating and capital funds have been underfunded in 19 of the last 25 years, making it hard to maintain existing stock. Meanwhile, nearly 200,000 units have been demolished or converted to Section 8 vouchers through the Rental Assistance Demonstration, contributing to the net loss from 1.3 million to 860,000 units.

What is the Rental Assistance Demonstration (RAD) program?

RAD allows public housing authorities to convert units to long-term Section 8 project-based rental assistance. Since 2012, nearly 200,000 units have been converted, and HUD can authorize up to 455,000 conversions total. The shift aims to leverage private financing for repairs but reduces the permanently owned public housing stock, raising concerns about long-term affordability and tenant protections.

How is public housing funded by the federal government?

Federal funding flows through two main channels: the Public Housing Operating Fund for daily operations and the Capital Fund for major repairs. Both have been underfunded in 19 of the past 25 years. Tenants generally contribute 30% of their income (after deductions) toward rent, with a minimum rent of up to $50, but these revenues are insufficient to cover escalating costs.

What reform proposals exist for public housing policy in the mid-2020s?

Key proposals include fully funding the Operating and Capital Funds to address the repair backlog, expanding the Housing Choice Voucher program to serve more families, and increasing new public housing construction. Other reforms focus on improving resident outcomes through supportive services, strengthening tenant protections in RAD conversions, and integrating public housing with other affordable housing strategies like LIHTC.

How does public housing compare to Housing Choice Vouchers in terms of resident outcomes?

Vouchers can enable moves to lower-poverty neighborhoods, potentially improving economic mobility, while public housing often concentrates poverty (45% of units are in high-poverty areas). However, voucher holders face landlord acceptance barriers, and public housing provides stable, deeply affordable rent (30% of income). Both approaches assist vulnerable populations: 56% of public housing households are headed by older adults or people with disabilities.