The Proposed Earnings Test for Federal Student Aid: What It Means for Public Policy

How outcome-based accountability reshapes higher education funding—and what MPA/MPP professionals should understand about the rulemaking process.

By Max SheltonReviewed by PAP Editoral TeamUpdated June 20, 202625+ min read

What you’ll learn in this article…

Graduates earning less than high school diploma holders for two years risk loss of federal loans and Pell Grants.

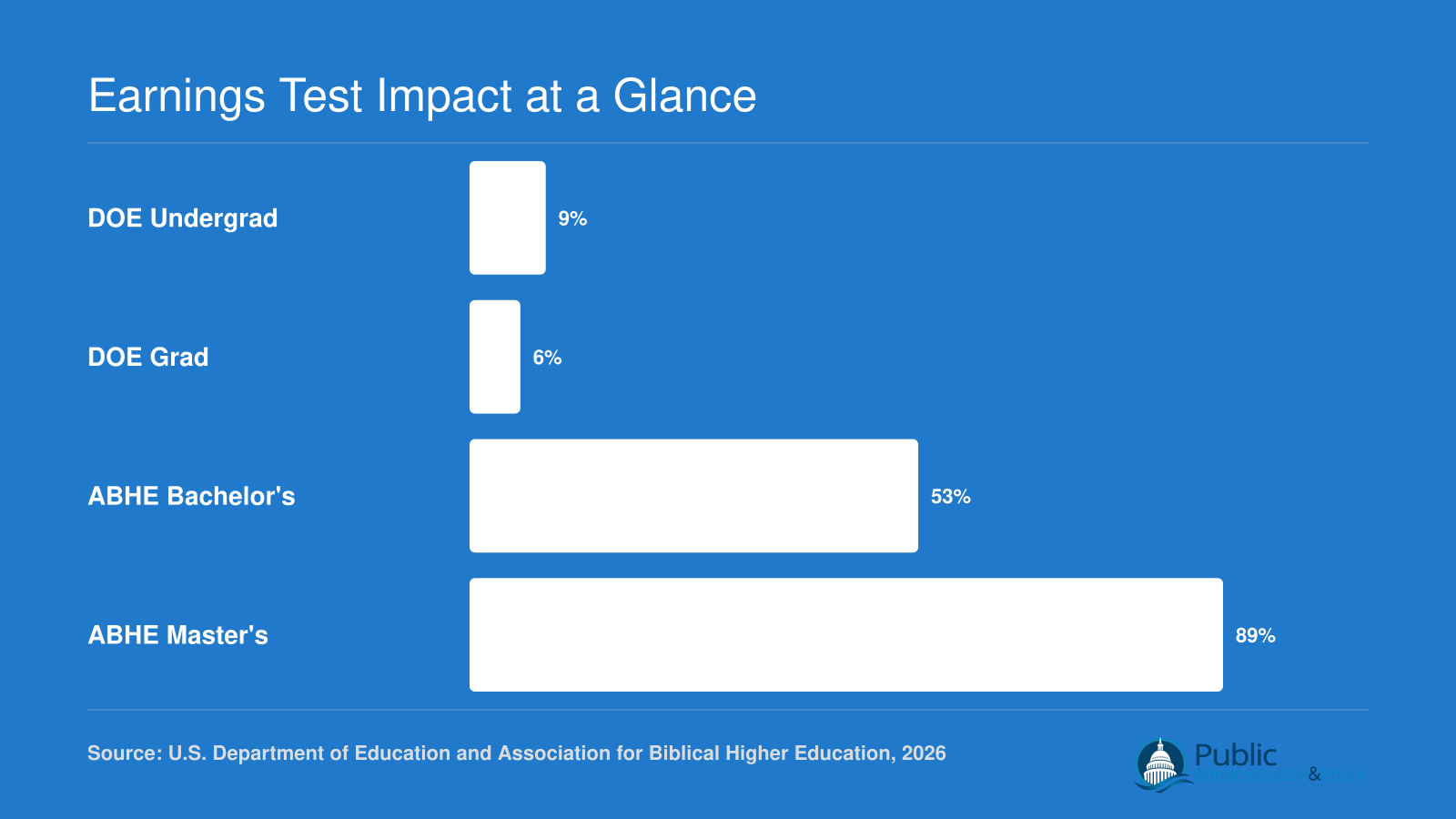

The Education Department estimates 9% of undergraduate religious studies programs fail, while religious colleges report 53%.

Over 8,500 public comments challenged the rule’s design, reflecting tensions between institutional mission and federal accountability.

The rule takes effect July 1, 2026, but past earnings-based regulations were struck down by courts.

For consumer advocates, the proposed earnings test is a shield: a way to cut federal aid from programs that leave graduates deep in debt with poverty-level wages. For religious colleges and beauty schools, it is a threat that could shutter programs whose value is not captured by salary benchmarks alone. More than 8,500 public comments landed in the Education Department's docket by May 2026, underscoring the stakes.

This rulemaking is a live case study in outcome-based accountability design, a central challenge for public policy professionals. As the test's mechanics spell consequences for a wide range of institutions, from Bible colleges to HBCUs, the debate reveals tensions between consumer protection, institutional mission, and regulatory feasibility. Past earnings-based accountability rules have been repeatedly blocked by courts, raising hard questions about whether this version will survive.

What Is the Proposed Earnings Test for Federal Student Aid?

The proposed federal earnings test is an accountability metric that compares the median earnings of graduates from any postsecondary program to a benchmark based on the earnings of high school diploma holders.1 In plain terms, if a program's typical graduate does not earn enough to clear a defined threshold above what someone without a college degree makes, that program risks losing access to federal student aid. The goal is to ensure that taxpayer-funded aid flows to programs that deliver measurable economic value to students.

Legislative Roots and Rulemaking Role

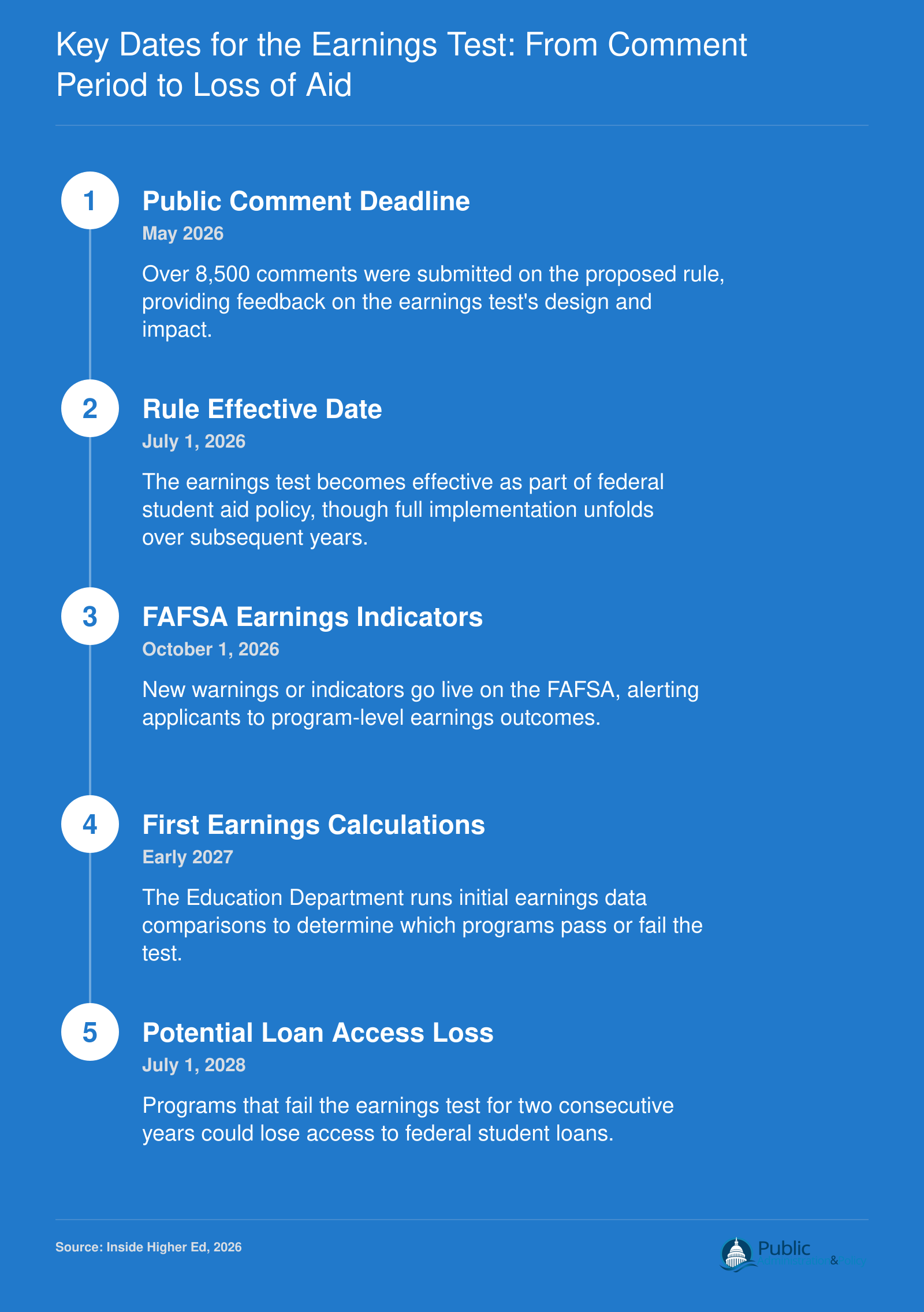

The earnings test originates from the One Big Beautiful Bill Act, a wide-ranging piece of legislation passed by Congress.1 The Act directed the U.S. Department of Education to craft a rule that ties federal student aid eligibility to earnings outcomes. In April 2026, the Department published a proposed rule2 and opened a public comment period that closed in May 2026 with over 8,500 submissions, as reported by Katherine Knott in Inside Higher Ed on May 26. The Department must now review those comments and issue a final rule; as of June 2026, the final regulation has not been published,3 though the statutory effective date remains July 1, 2026.

A Broader Scope Than Past Earnings Rules

Previous federal accountability efforts, notably the gainful employment regulations, applied only to for-profit and vocational programs. This new earnings test casts a much wider net. Under the proposal, every undergraduate and graduate program that participates in federal student aid , at public, private nonprofit, and for-profit institutions alike , would be subject to the same earnings threshold.1 A religious studies master's degree at a faith-based college, a nursing certificate at a community college, and a business degree at a large public university would all face scrutiny under the same metric. Understanding what public policy means in practice helps clarify why rules like this generate such broad debate across sectors.

Where Things Stand Now

Because the final rule had not been issued by the June 1, 2026 publication deadline and no formal delay has been announced,4 the timeline remains uncertain. If the rule is finalized and takes effect on July 1, 2026, the first full computation of program-level earnings would occur in early 2027.5 Programs that fail the test in two out of three consecutive years could eventually lose eligibility for federal student loans and, later, Pell Grants , though the earliest any aid loss could take effect is July 1, 2028.5 No legal challenges have been reported to date,4 but given the contentious history of earnings-based accountability, the path ahead is likely to be debated in both administrative and judicial venues.

How the Earnings Test Works: Thresholds, Data, and Methodology

The Move to Earnings-Based Accountability

The proposed earnings test introduces a new methodology for assessing program value, one that relies on publicly available earnings benchmarks and institutional data. At its core, the test compares the median earnings of a program's graduates against a threshold derived from the earnings of high school diploma holders. This approach shifts federal oversight from inputs like accreditation and cohort default rates to a direct outcome measure: does the credential pay off in the labor market? Understanding this shift is essential for anyone studying public policy making and the design of accountability systems.

Where the Data Comes From

The test draws on two primary federal data sources. The Bureau of Labor Statistics publishes national median earnings by educational attainment, including for individuals with only a high school diploma. These figures provide a broad benchmark against which programs can be measured. At the program level, the Department of Education uses the College Scorecard, which reports median earnings for students who received federal financial aid and are not currently enrolled. The Scorecard's cohort is defined as those who entered the institution and completed or withdrew, with earnings measured in the years following departure. Because the data only includes aid recipients, it may not fully represent all graduates, but it offers a consistent yardstick for comparison.

The Benchmark and the Warning Trigger

The earnings test sets a threshold, often a state-level or national median for high school graduates, and flags programs whose graduates' median earnings fall below that line. Some states publish their own labor-market data, which can be more granular and may serve as alternative benchmarks in the rulemaking process. The FAFSA process will integrate a lower-earnings indicator, alerting applicants when a program's median earnings are low relative to the threshold. This warning is not a prohibition; it is designed to inform student choice by surfacing potential financial risk before a student commits to a loan or grant.

Gaps and Ongoing Deliberations

Implementing the test requires resolving methodological questions about which earnings year to use, how to handle small programs with statistically unreliable data, and whether to adjust for regional wage differences. The public comment record shows strong interest in these details, with many commenters arguing that a poorly calibrated test could mislabel programs that serve low-income communities or prepare graduates for policy analyst careers. The Department is expected to clarify these mechanics as the rule moves toward finalization.

Programs that fail the earnings test for one year receive a warning. A second consecutive year of failure results in loss of federal student loan eligibility. Continued failure leads to loss of Pell Grant access at the institutional level, escalating consequences for programs and their students.

Which Programs and Institutions Are Most at Risk?

Department Estimates Versus Institutional Data

The Education Department's own analysis projected that 9 percent of undergraduate and 6 percent of graduate religious studies programs would fall short under the proposed earnings test.1 Those figures, drawn from large-scale federal datasets, suggest a manageable scope of concern. However, the Association for Biblical Higher Education (ABHE) challenged that assessment with starkly different numbers: 53 percent of bachelor's programs and 89 percent of master's programs in religious studies would fail.1 The discrepancy arises largely from data sources and granularity. The Department relies on aggregated post-graduation earnings records across broad program categories, whereas ABHE conducted institution-level surveys capturing outcomes for the precise programs its members operate. Small, specialized cohorts, often with graduates concentrated in pastoral or nonprofit roles, appear in federal data with earnings that are statistically diluted by larger programs. ABHE's survey removes that averaging, revealing far sharper vulnerability. The gap underscores how methodological choices in accountability metrics can produce vastly different pictures of risk.

Beyond Religious Studies: Other Vulnerable Programs

While religious studies became the focal point of public comments, the earnings test would cast a wide net. Beauty schools and cosmetology certificate programs consistently show low post-completion wages that would likely fall below the threshold measured against high school diploma holders. Fine arts, performing arts, and certain humanities credentials, especially at the certificate and associate levels, face similar exposure. Any program whose graduates routinely enter low-wage fields, social services, early childhood education, or public administration careers in local government may find itself flagged. The structural issue is not program quality but salary scales in the destination sectors. A licensed cosmetologist or early-career youth minister may earn less than the median for workers with only a high school diploma, not because the education lacked rigor, but because the labor market compensates those vocations modestly.

Why These Programs Fail: The Non-Economic Value Problem

The earnings test isolates one dimension of success: wages relative to a high school benchmark. For programs that intentionally prepare students for service roles, ministry, or community-based work, this framing misses the full return on investment. Graduates of religious studies programs often report high job satisfaction, meaningful community engagement, and non-monetary benefits that are entirely invisible to a wage comparison. Accrediting bodies and institutional leaders argue that accountability must acknowledge mission-driven outcomes. A policy that penalizes institutions for producing graduates in essential but lower-paid fields risks narrowing educational diversity and discouraging enrollment in programs that serve the public good without generating high personal earnings.

Consequences for Mission-Driven Institutions

Small, faith-based or specialized colleges rely heavily on federal student aid to sustain enrollment. The two-year failure clock means that a program failing the earnings test could lose access to federal loans first, and eventually Pell Grants.1 For institutions where the entire curriculum revolves around religious vocations, a single failing metric could decimate budgets and force closures. The ABHE data suggests that the majority of its member programs would be at risk, potentially disrupting access to ministry training nationwide. Beyond religious institutions, niche trade schools and community-based programs that serve underrepresented students also face existential threat. The earnings test, as currently framed, concentrates risk in institutions least able to absorb the loss of federal aid, raising urgent questions about equity and unintended consequences for educational access.

Earnings Test Impact at a Glance

The gap between the Department of Education's own estimates and those from the Association for Biblical Higher Education illustrates a central tension in the earnings test debate. While the government projects a modest share of programs at risk, faith-based institutions argue the real impact could be far more severe, raising questions about data transparency and methodological assumptions.

How Does the Earnings Test Affect Pell Grants and Student Loans?

The proposed earnings test introduces a tiered system of federal aid penalties that can strip program eligibility for student loans and, in severe cases, revoke an entire institution's access to Pell Grants.

The Consequence Ladder: Loans First, Pell Later

The rule establishes a progressive sanction model. After two consecutive years of failing the earnings threshold, a program loses eligibility to receive any new federal student loans.1 This is the first and most immediate trigger, directly cutting off Direct Subsidized, Unsubsidized, and PLUS loans for students in that program. If the program continues to fail in subsequent years, the Department of Education can escalate sanctions to include the loss of Pell Grant eligibility for that program. At that point, even the neediest students would be unable to use their Pell awards to pay for tuition in the flagged program.

The Institutional Trigger: When Entire Schools Lose Pell

Sanctions are not limited to individual programs. The proposed rule includes an institutional-level trigger: if a critical mass of programs at a single school fails the earnings test repeatedly, the entire institution's eligibility to participate in the Pell Grant program can be revoked. This "nuclear option" would effectively shutter many tuition-dependent colleges, particularly smaller private and career schools that lack diversified revenue streams. The Department would determine the threshold for institutional sanctions based on the share of failing programs and total enrollment in those programs, creating a high-stakes accountability mechanism that reaches far beyond isolated certificate programs.

Student-Level Impact: Low-Income Borrowers at Risk

For students currently enrolled in a failing program, the consequences are immediate and severe. They would need to either secure private loans, which often carry higher interest rates and less borrower protection, or transfer to another institution to maintain their federal aid eligibility. Transferring may not be feasible for students in specialized, location-bound, or mission-driven programs, and loss of Pell disproportionately affects low-income, first-generation, and minority students who are the primary beneficiaries of the grant. The policy thus risks punishing the very populations it aims to protect by removing their access to affordable higher education. Students weighing options in this environment may find that pursuing an affordable online MPA program offers a pathway less exposed to such accountability risks.

Corrective Periods and Appeals: What Options Do Institutions Have?

The draft rule provides several off-ramps before aid is permanently severed. After the first failure, a program enters a warning period and must submit a corrective action plan demonstrating how it will improve graduate earnings. Institutions can also appeal if they believe data errors or unique labor-market conditions skewed their results. However, past federal accountability efforts based on earnings metrics have been repeatedly challenged in court, and any appeals process will need to withstand legal scrutiny to be effective.1 The tight timeline, with the rule slated to take effect July 1, 2026, leaves little room for drawn-out negotiations.

The Irony: A Consumer Protection That Could Harm Students

The earnings test is designed to weed out low-value programs and protect students from unmanageable debt. Yet the most immediate effect for students in failing programs is the loss of their primary sources of financial aid. This creates a classic policy tension: the very mechanism meant to safeguard students may force them out of school or into worse financial arrangements. Public administrators and policy professionals must grapple with this irony as they weigh the test's potential to drive accountability against its capacity to exacerbate inequities in access.

Questions to Ask Yourself

How would you measure the societal value of a theology degree without defaulting to earnings?

Graduates often serve in community, spiritual, and nonprofit roles whose impact is not reflected in salary data. A pure earnings test risks penalizing programs that produce essential social goods.

What metrics could capture the public benefit of a social work degree beyond starting salary?

Social workers strengthen the safety net, improve mental health outcomes, and reduce strain on public systems. Earnings alone ignore these downstream effects on community well-being and government spending.

For fine arts graduates, how might policy weight creative contributions or cultural enrichment in accountability systems?

Cultural production enriches civic life but generates lower average earnings. Measurement that only tracks income may devalue contributions to community identity, innovation, and public dialogue.

Could a multi-dimensional scorecard incorporating civic engagement or volunteerism better reflect the full return on educational investment?

Single-metric tests miss non-monetary returns like leadership, public participation, and social capital. A broader framework might better align accountability with the diverse missions of higher education.

What the Public Comments Revealed: Over 8,500 Voices

The public comment period for the proposed earnings test closed in May 2026 after receiving more than 8,500 submissions from individuals, advocacy groups, institutions, and trade associations. This volume reflects the rule's potential to reshape federal student aid eligibility and the intense interest from stakeholders across higher education. The comments reveal deep divisions over whether the earnings test is a necessary consumer protection or a blunt instrument that threatens mission-driven programs.

A Tale of Two Perspectives

The comments largely split into two camps: those who see the test as overdue accountability and those who warn it will penalize programs with non-economic missions. Supporters argue the rule is essential to protect students, while opponents call it an existential threat.

Accountability Advocates: Protecting Students from Predatory Programs

Proponents emphasized that the earnings test would finally hold programs accountable for poor labor market outcomes. They argued that too many students enroll in expensive programs that fail to boost earnings above what a high school diploma would provide, leaving graduates with unmanageable debt. In their view, the test is a long-overdue safeguard against predatory practices, particularly in for-profit and certificate sectors. Many comments pointed to past scandals as evidence that federal aid should only flow to programs that deliver measurable economic mobility.

Institutional Stakeholders: Mission vs. Metrics

Opposition was especially vocal from religious colleges, beauty schools, small arts programs, and historically Black colleges and universities (HBCUs). These institutions argued that the earnings test overlooks the social, cultural, and spiritual value of their graduates. An earnings threshold that compares graduates to high school completers, they said, is ill-suited to assess programs training pastors, cosmetologists, or actors: careers where low entry-level wages do not equate to program failure.

The Association for Biblical Higher Education submitted its own analysis showing that 53% of bachelor's and 89% of master's religious studies programs would fail the test. Without Pell Grant and loan eligibility, many of these programs could not survive. Religious colleges warned of "devastating consequences" for their institutions and communities, highlighting that their graduates often enter public administration jobs or community service roles where they prioritize meaning over salary.

A Case Study in Participatory Rulemaking

For students of public administration vs public policy, the comment period itself is instructive. Over 8,500 comments demonstrate that federal rulemaking is not a closed technical exercise but a contested political arena. The volume and tone illustrate how agencies must balance Congressional directives with vigorous stakeholder pushback. Future administrators can learn from this process: robust outreach, data transparency, and careful response to comments are essential. The earnings test debate shows that even well-intentioned accountability metrics must navigate institutional diversity, constitutional concerns about federal overreach, and the practical limits of earnings data.

Policy Design Lessons: Balancing Accountability, Equity, and Litigation Risk

What legal and equity challenges could stop the proposed earnings test, and what does the history of gainful employment rules tell us about its survival?

A Litigation-Filled History: Gainful Employment from 2011 to 2025

Federal efforts to link student aid to earnings outcomes have landed in court almost every time. The 2011 gainful employment rule, effective July 1, 2011, required career training programs to meet a repayment rate threshold of at least 35 percent.1 A court partially vacated the rule in 2012, finding the 35 percent threshold arbitrary and capricious, though it upheld the Department of Education's statutory authority to regulate.1 The 2014 version switched to debt-to-earnings ratios2 and survived a 2015 challenge in APSCU v. Duncan, but its alternate earnings appeal pathway was struck down in 2017 on similar arbitrary-and-capricious grounds.2 The Trump-era 2019 rescission was itself litigated and remained in effect through 2021.2 The 2023 rule added an earnings premium metric alongside debt-to-earnings tests,3 and in 2025 a federal judge in Texas, Reed O'Connor, upheld it in AACS v. U.S. Department of Education.4 That post-Loper Bright validation signals a shift: courts are now more reluctant to second-guess agency expertise under the Higher Education Act.5

Legal Vulnerabilities of the 2026 Proposal

The current earnings test applies to all programs, not just for-profit or career-focused ones, which could cut both ways in court. Broader scope may strengthen the legal footing by making the rule less vulnerable to claims of targeting a disfavored sector. However, wrapping traditional academic programs into an earnings-premium framework invites lawsuits over whether the Department exceeded statutory authority under the HEA, particularly from religious and liberal arts institutions whose missions are not primarily vocational. The 2023 win shows that carefully documented agency reasoning can withstand arbitrary-and-capricious review, but a single-metric test that ignores field-of-employment variation might be more fragile. Expect challengers to argue that comparing all graduates to high school earnings is arbitrary for programs that produce clergy, educators, or social workers, fields society values beyond wages.

Equity Implications: Disproportionate Impact on Public-Service Programs

The earnings test threatens to penalize institutions that serve low-income and minority students precisely because their graduates enter vital but lower-paying fields. Past gainful employment litigation never centered on equity per se, but data already shows religious studies programs topping the failure list, and public policy making analysis of the comment record reveals deep concern from minority-serving institutions. HBCUs, which produce a disproportionate share of Black teachers and social workers, could see programs flagged simply because state and nonprofit pay scales lag private-sector earnings. The test creates a perverse equity trap: an accountability system designed to protect students may shut down the very programs that offer economic mobility through public service.

The Metric-Design Trap: Single-Measure Systems and Perverse Incentives

Outcome-based accountability is a core public-administration principle, but any single metric invites gaming. If graduation-rate pressure taught us "cream-skimming," an earnings-only test could push colleges to recruit students from higher-earning backgrounds and steer them away from ministry, education, and social work. It may also accelerate program closures in rural and underserved areas where local wages are low, deepening regional inequality. Policy designers must weigh whether an earnings premium threshold actually signals program quality or simply reflects occupational choice and geography.

Complementary Metrics: Beyond the Earnings Premium

Alternatives already tested in earlier rules offer a more nuanced picture. Debt-to-earnings ratios, central to the 2014 and 2023 rules,3 capture whether a graduate can repay loans without excessive burden. Loan repayment rates measure actual borrower success. Employment-in-field rates address whether the credential led to a relevant job. Student satisfaction and post-completion surveys could add a missing human dimension. A composite index that allows programs to demonstrate value along multiple dimensions would better align with public administration's balanced-scorecard approach while reducing legal vulnerability and equity blowback.

Equity Implications: MSIs, HBCUs, and Low-Wage-Field Programs

The earnings test promises to shield low-income students from debt that leads to poverty, yet the very institutions most committed to serving these communities, minority-serving institutions (MSIs) and historically Black colleges and universities (HBCUs), face disproportionate risk.

The Equity Case for the Earnings Test

Proponents argue that the test is a consumer protection essential. With 6% of all programs projected to fail,1 the regulation aims to prevent students from taking on federal debt for credentials with little labor-market payoff. By introducing a low-earnings warning on the FAFSA,2 the policy nudges students away from programs that could trap them in unmanageable debt. For low-income students who disproportionately rely on Pell Grants and loans, the measure addresses an information asymmetry that can lead to life-altering financial harm. In theory, it also pressures institutions to improve or shut down low-performing programs, raising the floor for all students.

The Disproportionate Burden on MSIs and HBCUs

Critics point to a deeply inequitable fallout. HBCUs and other MSIs are heavily dependent on Title IV federal aid and disproportionately enroll Pell-eligible students.3 Their program portfolios skew toward fields that produce modest but socially vital wages: teacher education, social work, and public administration. Projections indicate that undergraduate certificate programs, often concentrated at community colleges and for-profit institutions serving low-income and minority populations, face a 29% failure rate, compared to 6% nationally.1 By linking aid eligibility to earnings relative to high school graduates or BA holders,4 the test penalizes institutions that deliberately serve low-income communities and first-generation students, undercutting their very mission.

Low-Wage Public-Service Fields in the Crosshairs

Fields aligned with public service careers in federal civil service, including social work, early childhood education, counseling, library science, and ministry, all register as high risk under the proposed thresholds.5 Graduate programs in these areas must clear state median earnings of BA holders aged 25 to 34, a bar that often exceeds the wages schools and nonprofits can pay.4 Yet these are precisely the roles that public administration and policy students may pursue. The irony is sharp: a test designed to protect consumers may steer the most dedicated future public servants away from the programs that prepare them.

Structural Wage Gaps and the Blind Spots of Metrics

The earnings test also fails to account for structural wage gaps tied to race, gender, and geography. Black and Latino graduates, for example, face persistent pay disparities even with the same credentials. HBCU graduates are more likely to work in communities where wages are lower, but their social impact may be outsized.3 By using a blunt earnings threshold, the rule ignores these dynamics, risking the defunding of institutions that are engines of economic mobility, simply because their graduates' salaries don't align with a narrow, state-level benchmark.

How Public Administrators Can Engage With the Rulemaking Process

Over 8,500 public comments poured into the Education Department's rulemaking docket by the time the comment period closed in May 2026, signaling deep national interest in the proposed earnings test. This volume reflects how federal student aid policy directly intersects with the work of public affairs specialists in higher education, workforce development, and consumer protection.

The Notice-and-Comment Framework

The proposed rule follows the Administrative Procedure Act (APA), which requires agencies to publish a Notice of Proposed Rulemaking, accept public input, and issue a final rule with a reasoned response to significant comments. The earnings test proposal is currently in the comment-review phase; a final rule must respond to the record before taking effect (currently slated for July 1, 2026). Public administrators should understand that their substantive, well-documented comments become part of the administrative record and can shape legal defensibility.

Concrete Steps for Public Administrators

Submit individual comments: Any interested person can file through Regulations.gov. Effective comments cite evidence, propose alternatives, and explain practical impacts on institutions or students.

Organize institutional responses: Public affairs officers at colleges, state higher education agencies, and workforce boards can coordinate data-driven submissions, especially if the institution or program serves low-income or nontraditional students.

Seek a seat at negotiated rulemaking: After public comment, the Department may convene a negotiated rulemaking committee to build consensus. Administrators with policy expertise can volunteer through their professional networks.

Mobilizing Through Professional Associations

Associations like NASPA: Student Affairs Administrators in Higher Education, the American Council on Education (ACE), and the National Association of Student Financial Aid Administrators (NASFAA) are actively coordinating comments and advocacy. They often provide templates, host briefings, and arrange meetings with Education Department officials. Joining these efforts amplifies individual voices and ensures practitioners' on-the-ground knowledge reaches rule writers. Professional development in public policy can sharpen the technical communication skills needed to make comments that genuinely influence rulemakers.

Navigating Legal Challenges and Implementation

Past earnings-based accountability rules have been struck down in court for exceeding statutory authority or having arbitrary metrics. If the final rule is challenged, public administrators may be called to interpret the rule during a stay, manage compliance readiness, or produce institutional data. Understanding the rule's rationale and the administrative record helps administrators adapt operations swiftly if parts of the rule survive.

Why Engagement Now Matters

The rulemaking process is not a closed door. The Department must consider all timely comments. By contributing data on program costs, graduate outcomes, and the potential unintended consequences of the test, public administrators help craft a regulation that balances accountability with educational access. The window for formal comment may have closed, but ongoing engagement through advisory committees, congressional outreach, and association leadership still influences the final shape of the rule.

Key Dates for the Earnings Test: From Comment Period to Loss of Aid

The earnings test rulemaking follows a compressed timeline, with major milestones over the next two years. Public administrators should monitor these dates as implementation proceeds, recognizing that litigation or administrative delays could alter the schedule.

Frequently Asked Questions About the Federal Earnings Test

The proposed federal earnings test has generated widespread discussion among students, institutions, and policy professionals. The following questions and answers distill key aspects of the rule and its potential impact on federal student aid.

What is the federal earnings test for student aid?

It is an accountability metric proposed by the U.S. Department of Education under the One Big Beautiful Bill Act. The test compares a program’s graduates’ earnings to the median earnings of high school diploma holders. Programs where graduates fail to exceed that threshold for two consecutive years may lose access to federal student loans and eventually Pell Grants.

What is the FAFSA earnings warning and how does it affect students?

If a student’s potential program fails the earnings test, the FAFSA may display a warning that the program’s graduates do not reliably out-earn high school diploma holders. This notice is designed to inform enrollment decisions. Students attending a failing program could risk losing federal aid eligibility if the program is ultimately sanctioned.

How does the earnings test affect Pell Grants and student loans?

A program that fails the test for two consecutive years first loses eligibility for federal student loans. If it continues to fail, it may subsequently lose access to Pell Grants. This phased loss of aid is intended to protect students and taxpayers from programs with persistently poor labor-market outcomes, but it could also limit college access.

Which colleges and programs are most likely to fail the earnings test?

Programs in fields with historically lower earnings are at higher risk. Department data indicates 9 percent of undergraduate and 6 percent of graduate religious studies programs would fail. The Association for Biblical Higher Education reported that 53 percent of bachelor’s and 89 percent of master’s religious studies programs would fail, and beauty schools also raised concerns.

How is the earnings test different from previous gainful employment rules?

Past gainful employment regulations applied primarily to career training programs at for-profit and certificate-granting institutions, using debt-to-earnings ratios. The new earnings test applies more broadly, uses a simple earnings comparison to high school graduates, and ties directly to loan and Pell eligibility. It was crafted to be legally defensible after earlier rules were blocked by courts.

Can institutions appeal if they fail the earnings test?

The final rule is expected to include an appeals or reconsideration process, allowing institutions to challenge data or demonstrate mitigating circumstances. During rulemaking, stakeholders can shape these procedures. Historically, similar accountability metrics have allowed corrections for data errors or program-level improvements. Institutions may also pursue legal challenges if necessary.

How can I submit a public comment on the earnings test rule?

When the Education Department opens a rulemaking docket, comments can be submitted at Regulations.gov by searching for the relevant docket number. The public comment period for the current proposal closed in May 2026 with over 8,500 submissions. For future rulemaking phases, monitor the Federal Register or the department’s website for opportunities to engage.